April brought a subtle shift in the Downtown Minneapolis market — one that feels more like a seasonal delay than a structural change. While activity levels held relatively steady compared to last year, colder-than-usual weather played a meaningful role in slowing momentum, particularly in buyer movement and showing activity.

Even so, the underlying story remains consistent: this is a market that is steady, yet selective.

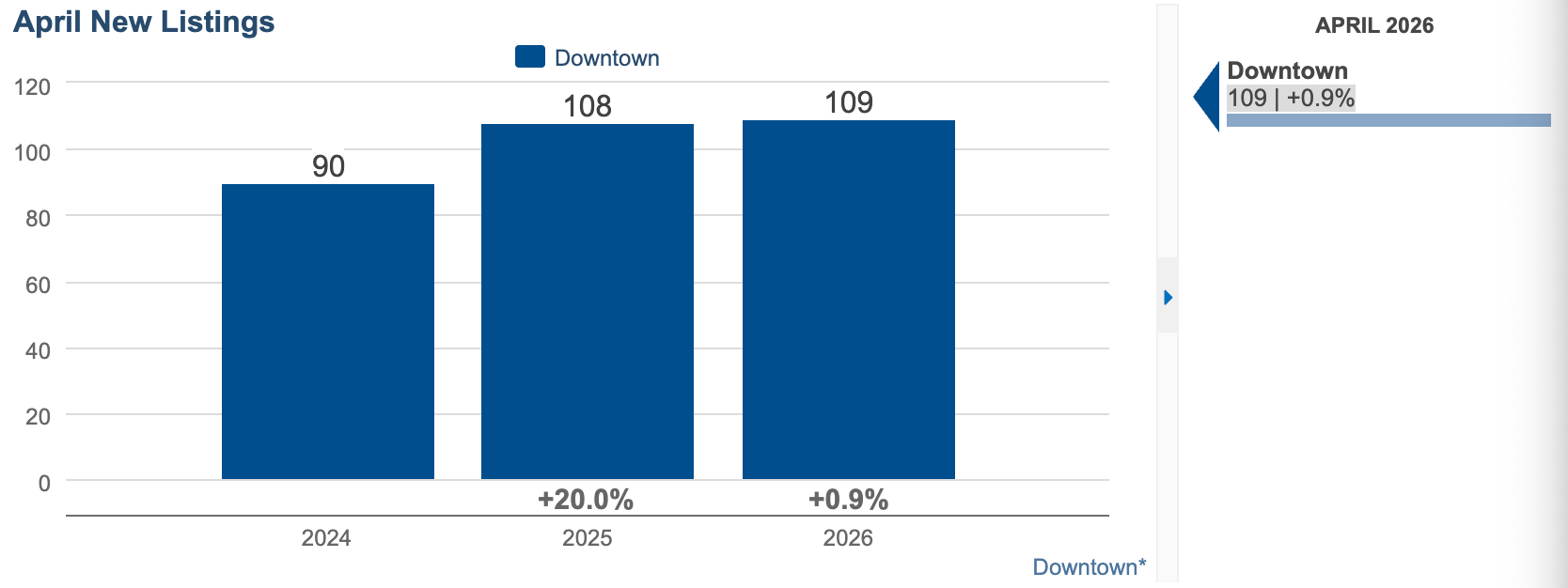

New Listings

April 2026: 109 (+0.9% YoY)

New listings were essentially flat year-over-year, signaling a level of seller confidence returning to the market. Unlike the slower start to the year, April showed that homeowners are willing to list — though often with careful timing and preparation.

Inventory is building at a measured pace, offering buyers more choice without tipping into oversupply.

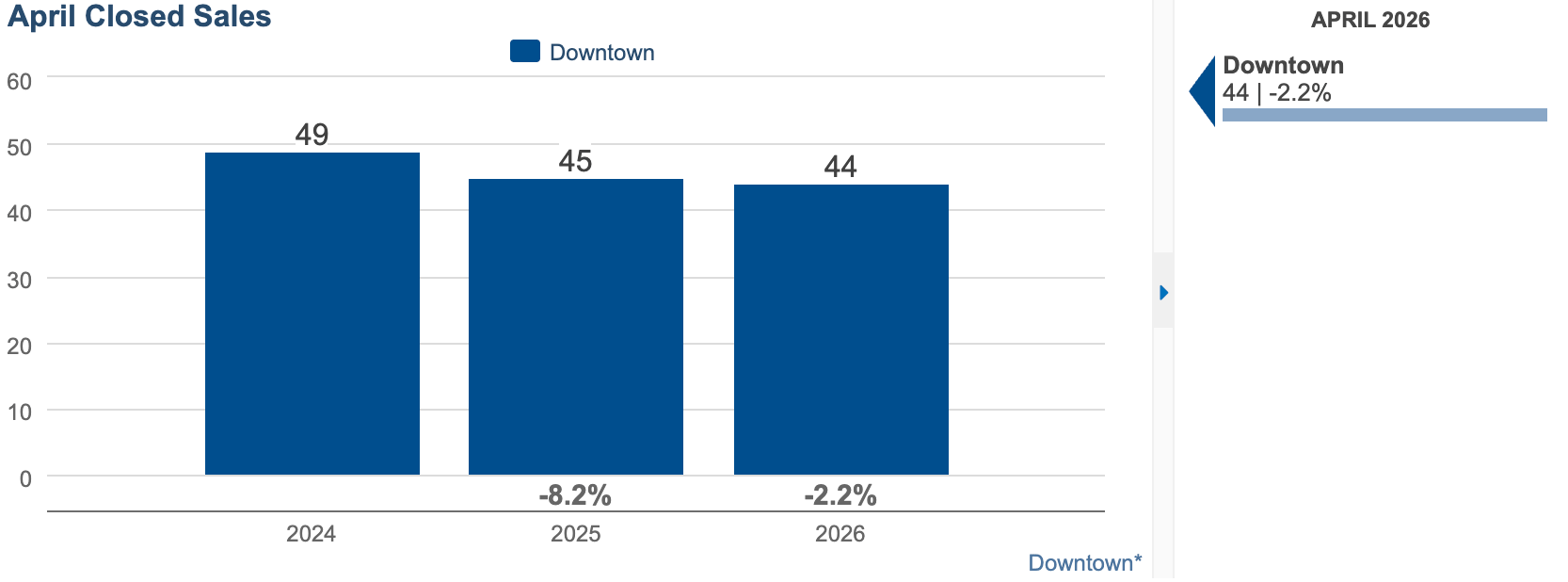

Closed Sales

April 2026: 44 (-2.2% YoY)

Closed sales held relatively close to last year’s levels, with only a slight dip. This suggests that while conditions may feel slower, transactions are continuing at a fairly stable pace.

Buyers remain active — just more deliberate. The urgency of past markets has softened, replaced by a more thoughtful approach to decision-making.

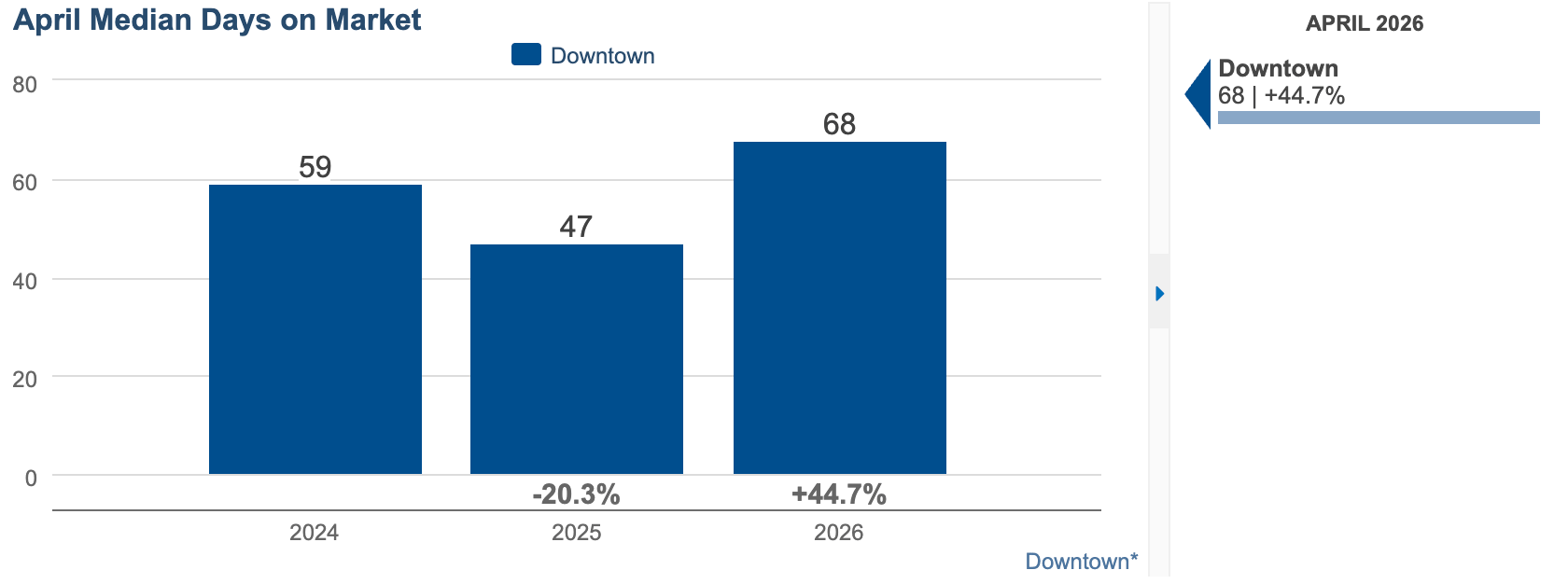

Median Days on Market

April 2026: 68 days (+44.7% YoY)

Days on market increased notably compared to last year, due in part to an unseasonably cold April that delayed showings, foot traffic, and overall engagement.

This longer timeline doesn’t necessarily reflect weaker demand, but rather a temporary slowdown in market flow. As weather improves, we often see this metric correct itself.

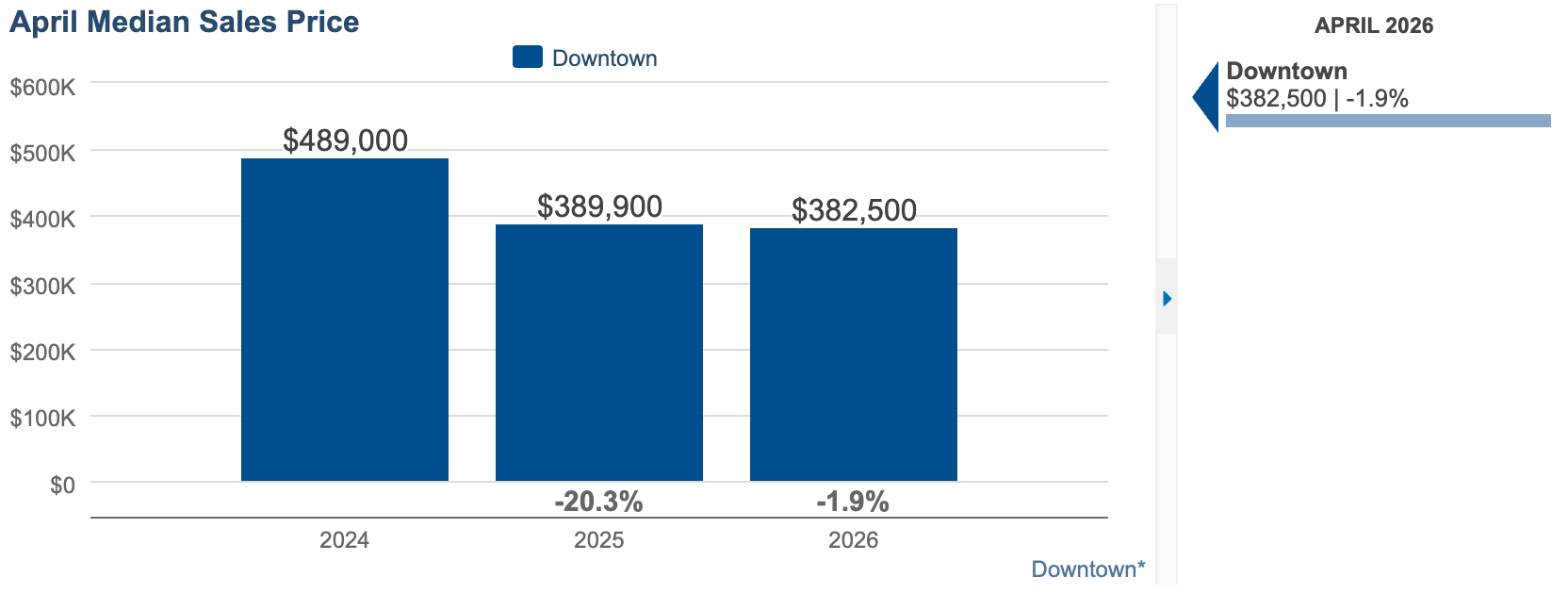

Median Sales Price

April 2026: $382,500 (-1.9% YoY)

The median sales price saw a slight dip, continuing the theme of minor adjustments rather than major shifts. Pricing remains relatively stable, with small fluctuations largely influenced by the mix of properties selling.

Well-located, well-updated homes continue to command strong interest and solid pricing.

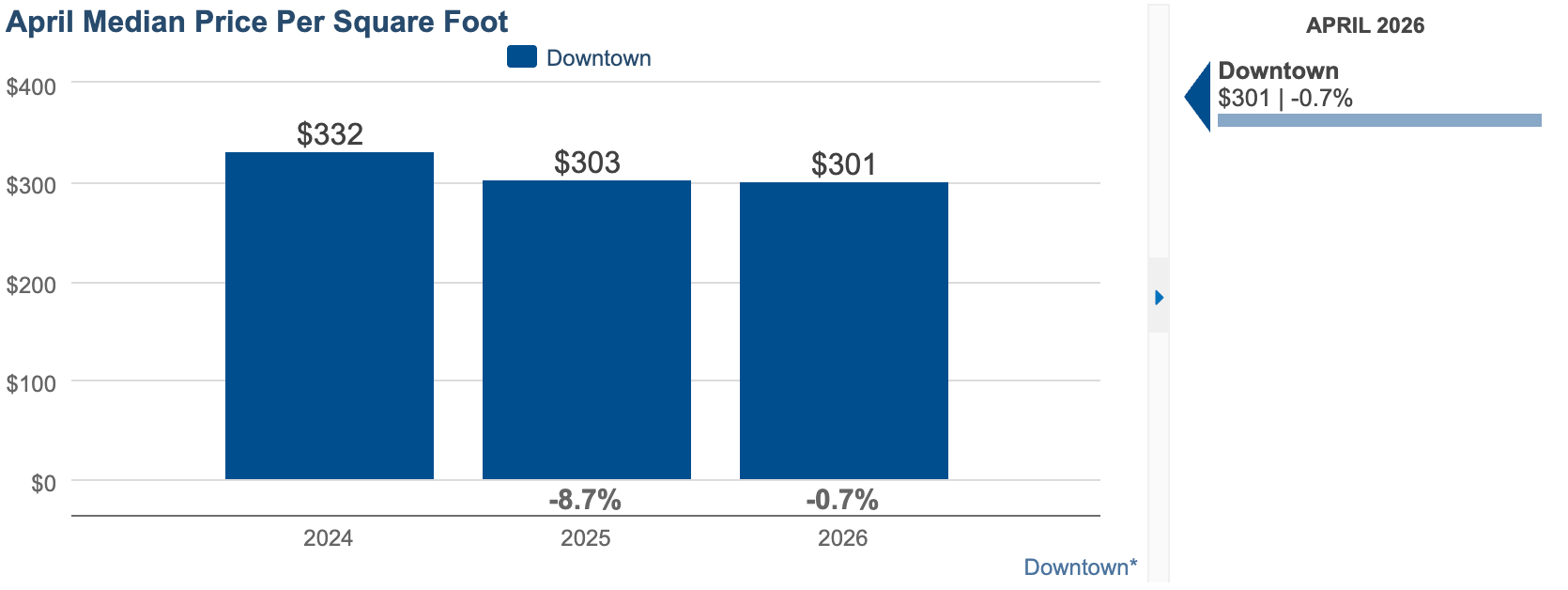

Median Price per Square Foot

April 2026: $301 (-0.7% YoY)

Price per square foot remained nearly unchanged, reinforcing the idea that underlying property values in Downtown Minneapolis are holding steady.

Buyers are still willing to pay for quality and location — but with a sharper eye toward overall value.

The Broader Picture

April reflects a market that is stable, with seasonal factors temporarily influencing pace. The combination of steady inventory, near-flat pricing, and slightly extended timelines paints a picture of balance.

For Downtown Minneapolis, this is a nuanced moment. The appeal of urban living — walkability, proximity to the river, vibrant neighborhoods — remains strong. But today’s buyers are engaging more thoughtfully, weighing timing, value, and long-term fit.

This is not a market driven by urgency. It’s one shaped by intention.

For sellers, success lies in preparation and realistic pricing. For buyers, there is opportunity in the form of time, choice, and negotiating room — especially during moments when external factors, like weather, create temporary pauses.