In October 2024, the Minneapolis real estate market showed a blend of price growth and signs of the shifting seasons. Median sales prices have risen notably, reflecting strong demand, yet shifts in other key metrics like longer days on market, fewer closed sales, and an increase in new listings point to a more balanced and potentially stabilizing market. This data highlights both ongoing demand and emerging buyer caution as inventory levels and affordability come into focus.

Here’s a closer look at the key trends shaping the market this past October...

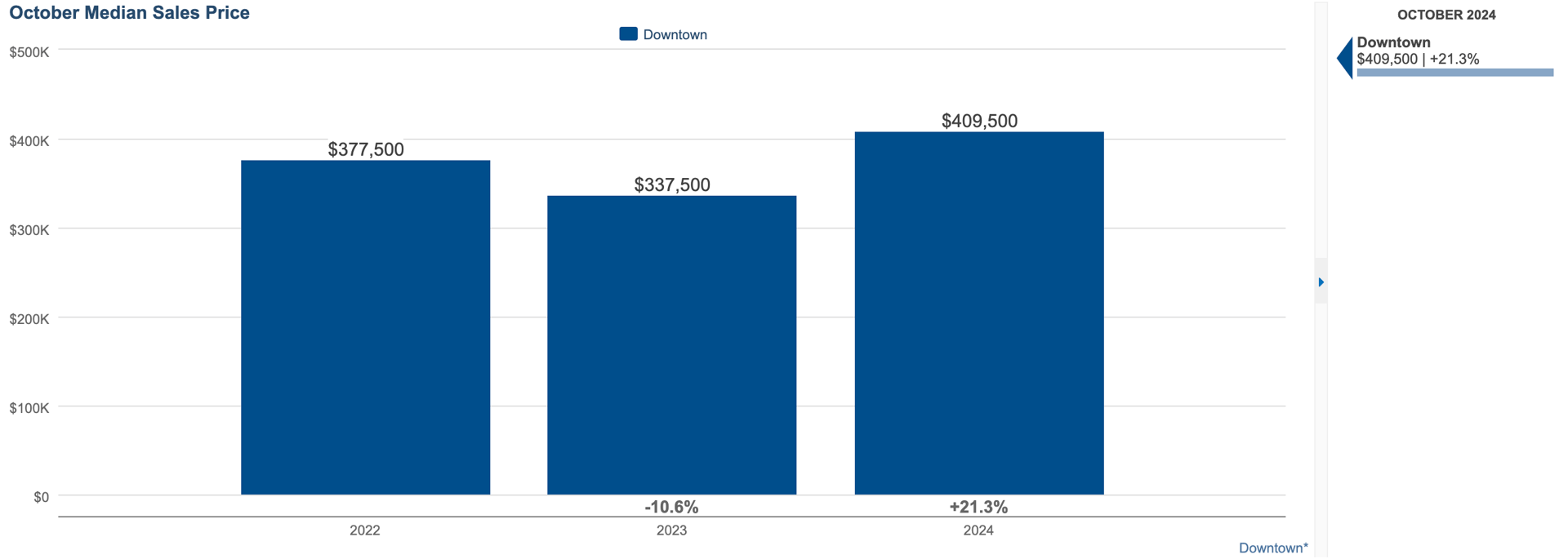

Median Sales Price: The median home price in Minneapolis rose significantly to $409,500 in October 2024—a 21% increase over last year. This sharp rise in prices, despite fewer transactions, suggests that there’s still strong demand in certain segments, even though the overall volume of sales has decreased.

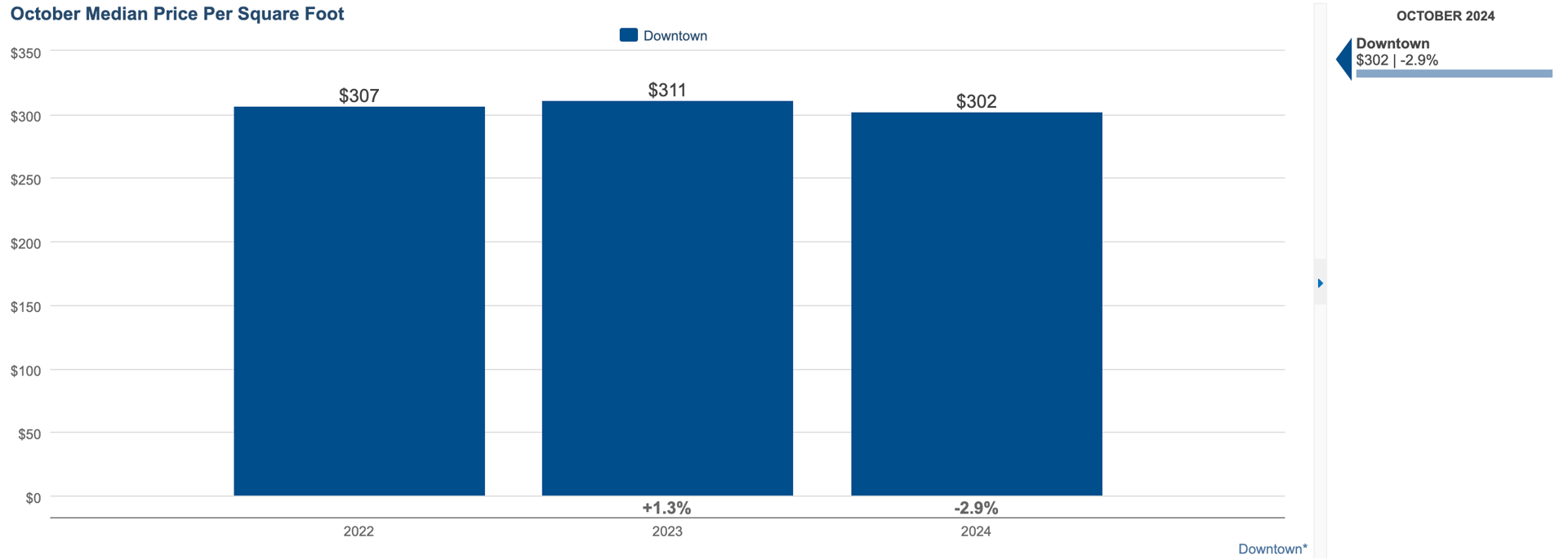

Price per Square Foot: Although the overall median price is up, the price per square foot has actually declined by about 3% from last October, holding steady with September’s rate of $302. This might indicate that buyers are opting for larger, possibly more affordable properties, balancing the higher overall prices with cost per square foot. It could also signal a selective trend in which high-value homes are selling, but without as much upward pressure on price per square foot.

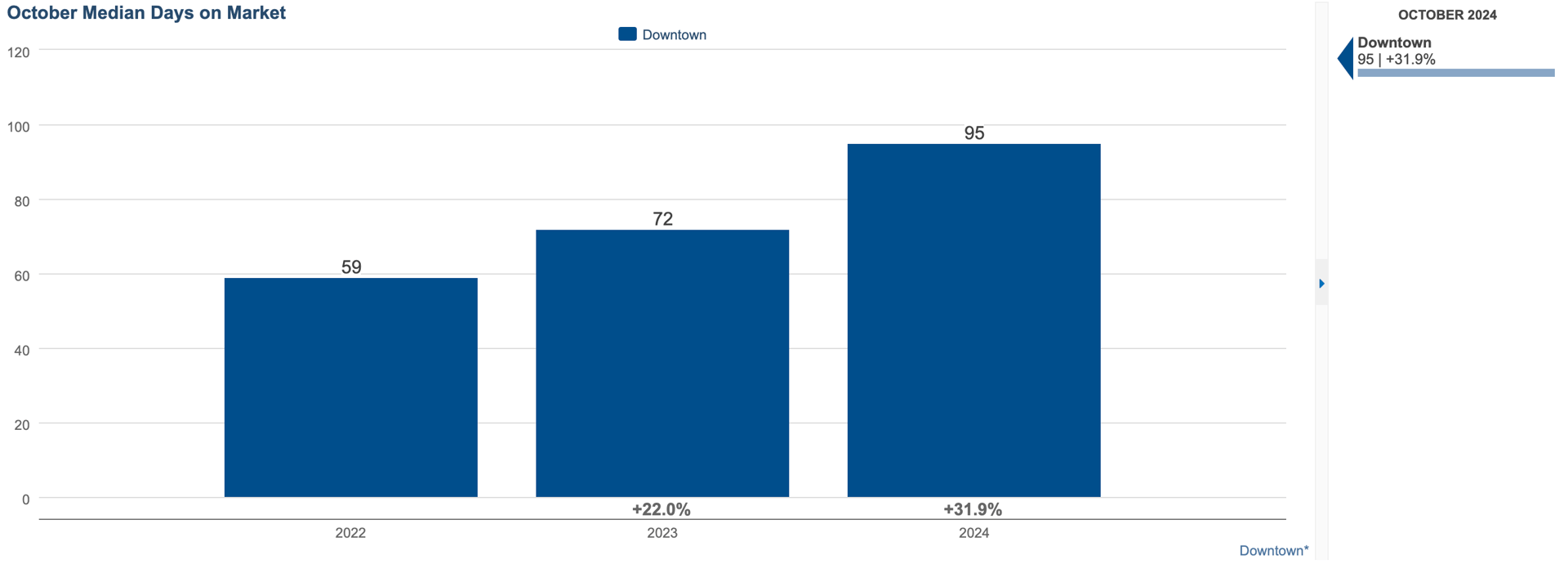

Median Days on Market: With a median of 95 days on market—32% longer than last year—homes are taking more time to sell, despite the increase in prices. This slower pace of transactions could reflect a more cautious or discerning buyer base. Buyers might be negotiating more carefully or taking time to consider options as more listings come to market and higher prices challenge affordability.

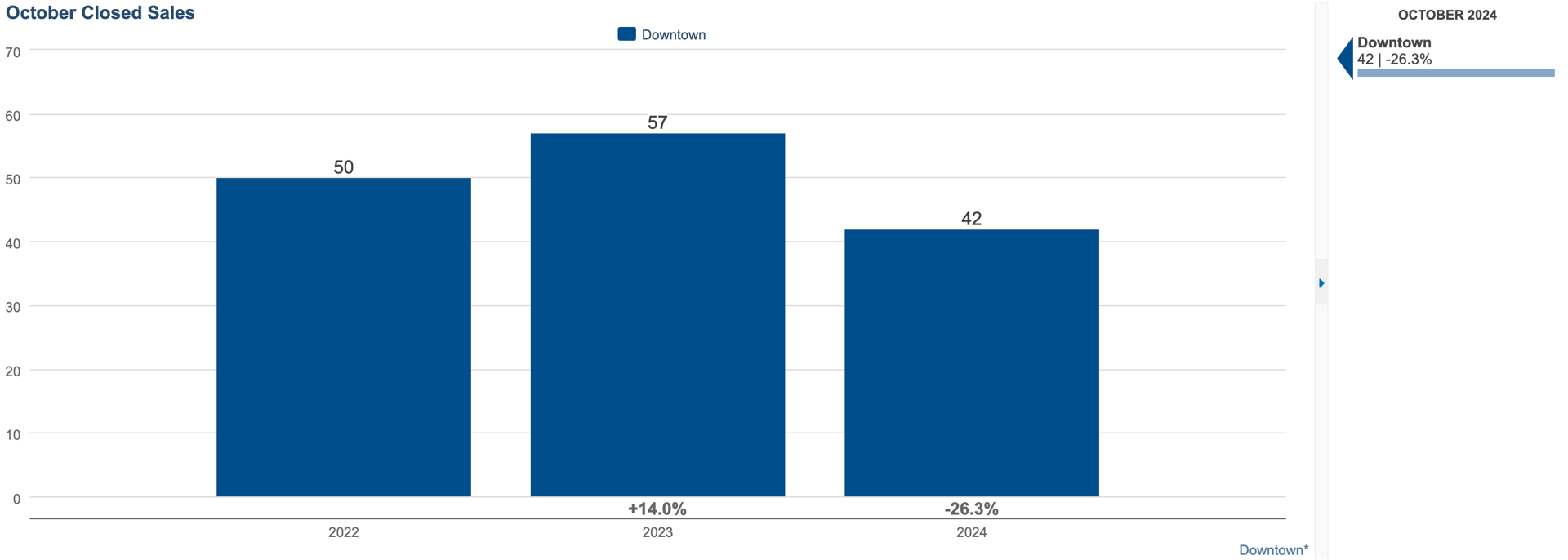

Closed Sales: The number of closed sales has dropped significantly, down 26% from last year with only 42 homes closing in October. The decline in completed transactions, even with higher prices, suggests that some buyers may be priced out or hesitant in a market where prices have risen, but where options and longer time on market may not fully align with their budgets or preferences.

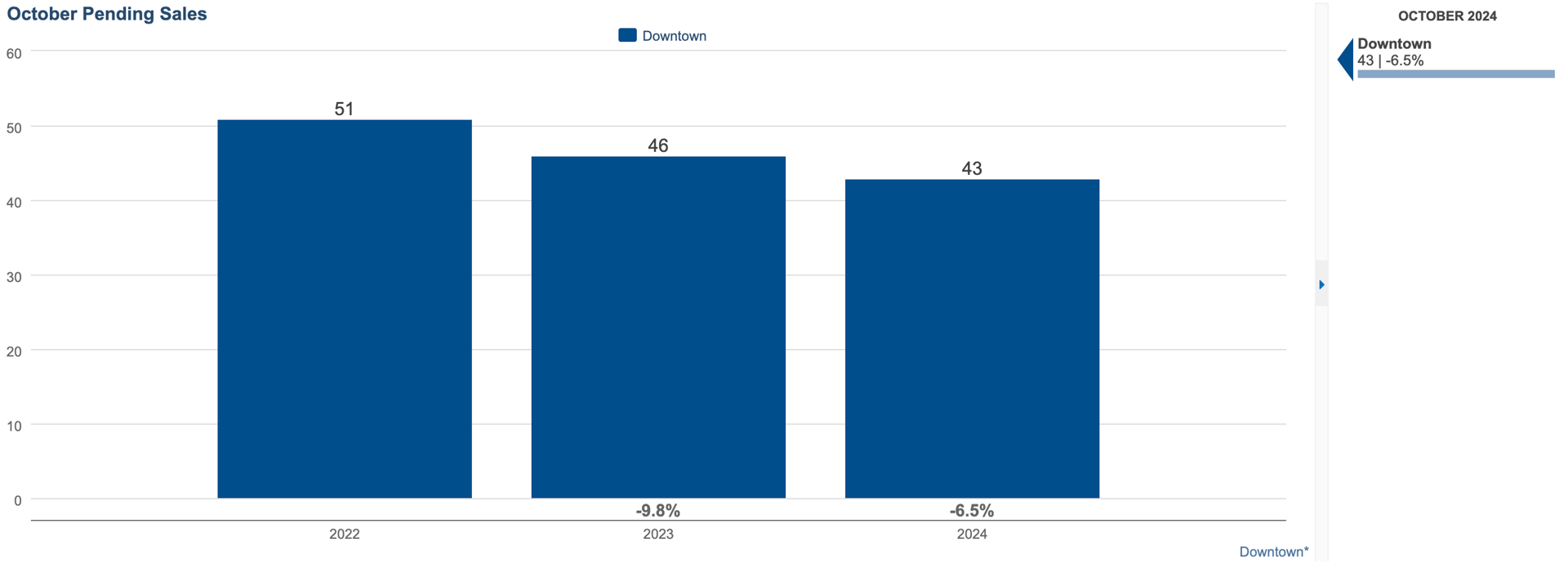

Pending Sales: Pending sales are also slightly down, about 6% from last October, totaling 43 homes. Fewer pending transactions indicate that, while some buyers are still actively making offers, the slower pace of closed sales may lead to increased inventory in the coming months, potentially tempering price growth if the trend continues.

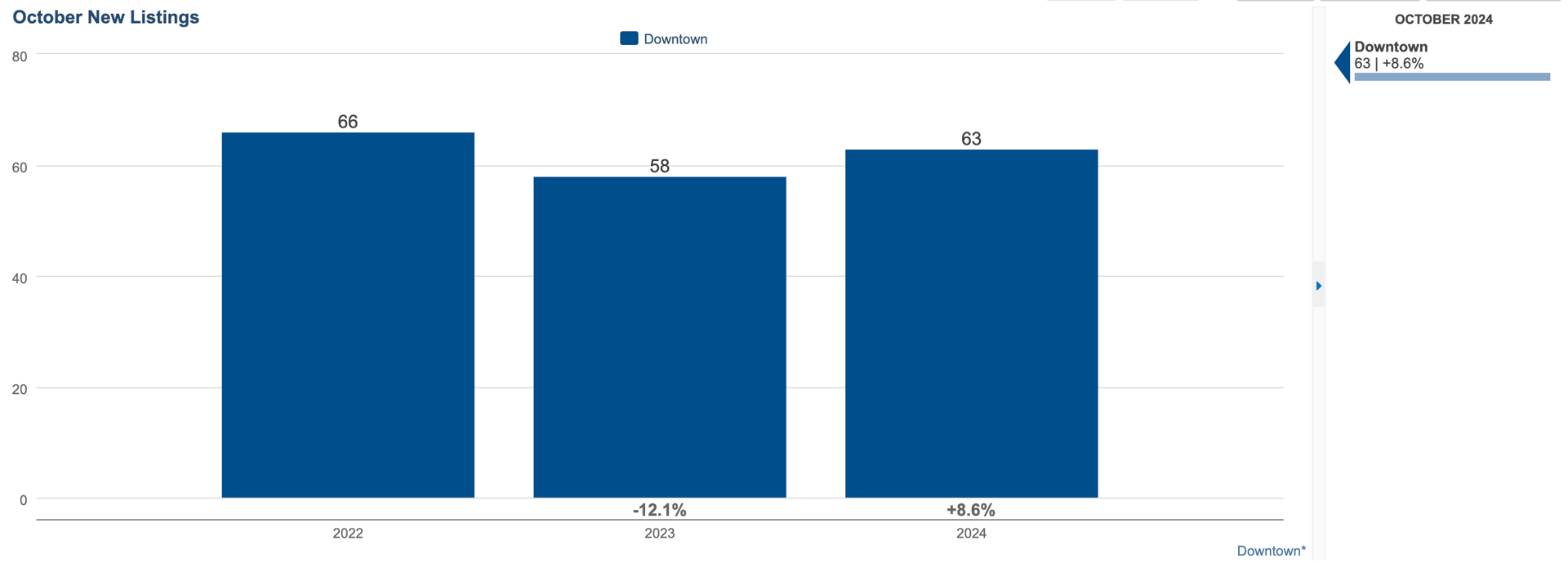

New Listings: New listings saw a modest increase of about 9%, totaling 63 homes in October. This rise in listings provides buyers with more options, which may be contributing to the longer days on market and a more selective buyer approach. An increase in listings amid high prices and fewer sales could also signal a market shift toward greater balance, where supply is gradually catching up with demand.

Bottom line?

Buyers seem to be more cautious, and with an increase in supply, sellers may need to adjust their strategies to meet evolving buyer expectations.

This comes down to pricing & presentation. Ensure you consider these important factors when assessing and reassessing your listing.

REACH OUT TO DISCUSS HOW THESE NUMBERS AFFECT YOUR MARKET TIMING AT [email protected]

Data retrieved from the NorthStarMLS via map of Downtown Minneapolis Neighborhoods including: Loring Park, Elliot Park, Downtown West, Central Minneapolis, North Loop, East Town, Mill District, Nicollet Island, St. Anthony West, and Marcy-Holmes.

HAVE QUESTIONS ABOUT DOWNTOWN MINNEAPOLIS OR SURROUNDING REAL ESTATE MARKETS?

Contact our team by call, email, or submitting a form at: https://lynnburnrealestate.com/