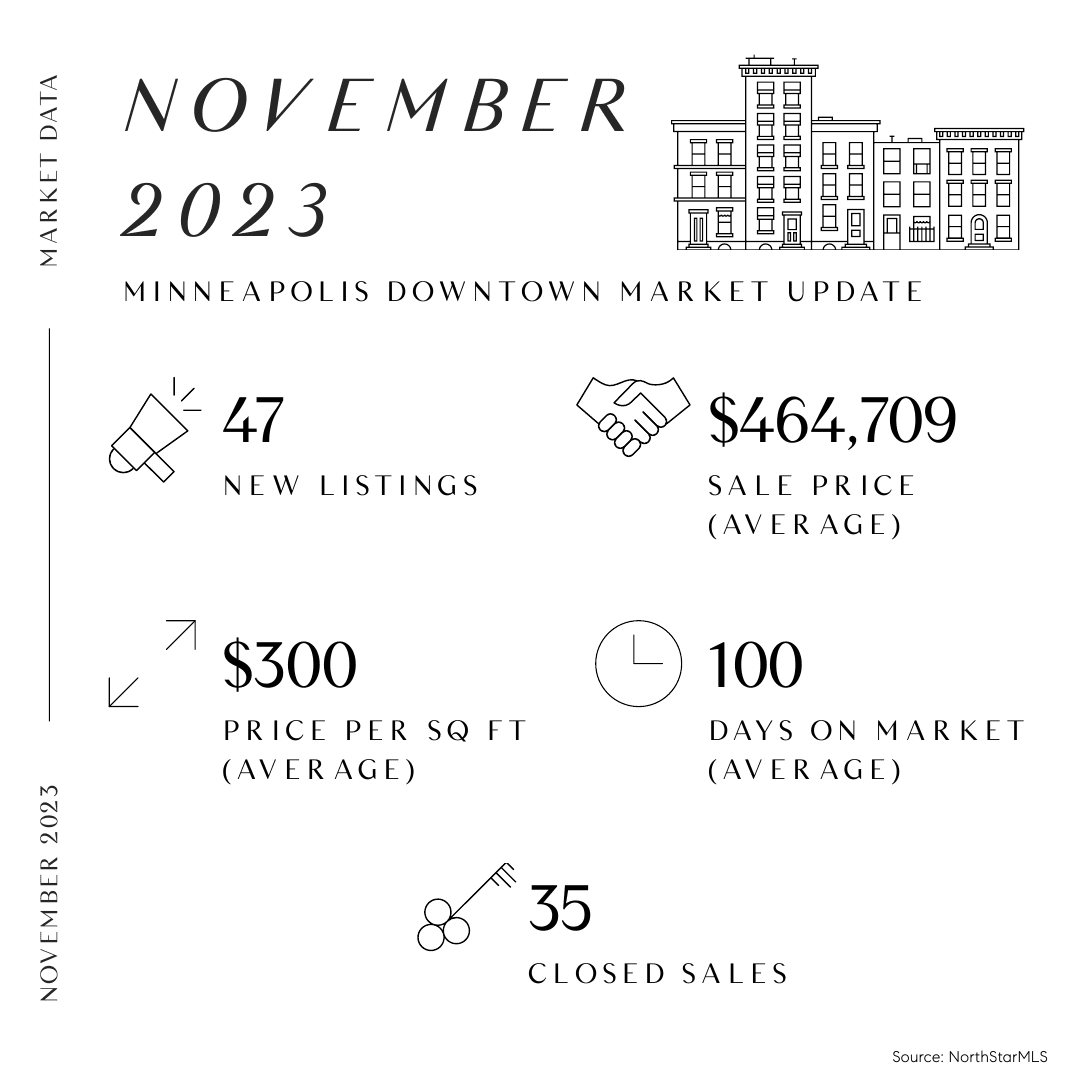

November showed an interesting picture compared to the same time last year… let’s dive in:

- New Listings are up 23.7% (27 in November this year vs. 38 in November 2022) giving buyers more options and highlighting the need for entering the market with expert staging and marketing.

- Pending Sales are up 26.1%, and closed sales are down 10.3% which are typically a trailing indicator of performance from October’s and prior months’ new listings.

- The Average Price Per Square Foot is Down 4.8%. It should also be noted that price per square foot is influenced by many factors including those highly changeable such as home upgrades.

- The Average Sales Price is Down 13.3% When the average price per square foot is down much less than the overall average price, it can be interpreted that the average prices of homes on the market were in a slightly lower bracket than the average in 2022, and the price per square foot indicator becomes a more valuable data point.

- Average Days on Market is up 19%.

The winter market is an excellent time to be a buyer - with less competition allows the ability to search with confidence.

Reach out to me today to start your search and Sellers... it’s time to prep for listing now for the turn of the year!

Data retrieved from the NorthStarMLS 12/4/2023 with some variation anticipated between sources and interpretation.

Data retrieved from the NorthStarMLS via map of Downtown Minneapolis Neighborhoods including: Loring Park, Elliot Park, Downtown West, Central Minneapolis, North Loop, East Town, Mill District, Nicollet Island, St. Anthony West, and Marcy-Holmes.

Do you have questions about Downtown Minneapolis or surrounding real estate markets?

Contact our team by call, email, or submitting a form at: https://lynnburnrealestate.com/